Follow our ongoing coverage of WWE’s Q3 earnings report and conference call on Thursday, beginning at 4:00pm ET, both here at wrestlenomics.com and on Twitter @BrandonThurston. Anyone may view WWE’s public filings and listen to Thursday’s 5:00pm conference call at corporate.wwe.com.

Subscribers at patreon.com/wrestlenomics get access to a live stream discussion with Brandon Thurston at 8pm ET Thursday night, covering WWE’s Q3 earnings report.

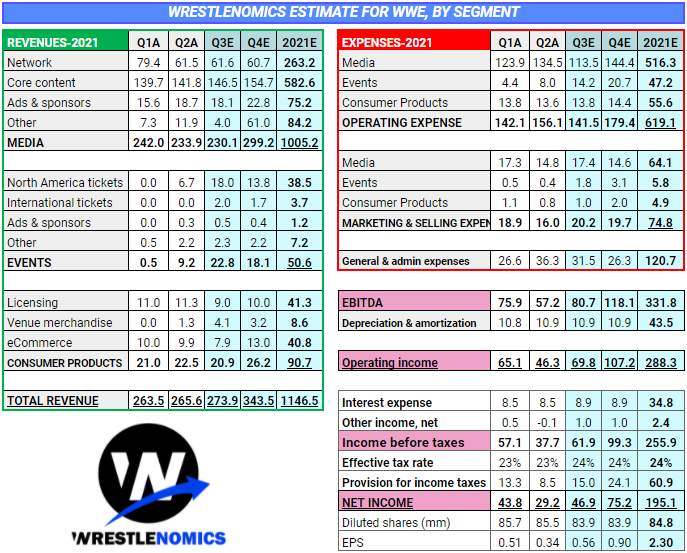

WWE’s third quarter earnings report on Thursday will be the first since the return to touring, which resumed on July 16.

My estimate of earnings per share ratio for the quarter ($0.56) is well above the highest of 11 analysts. Analysts’ mean EPS is $0.35, the low is $0.27, and the high is $0.39, according to a Refinitiv Stock Report.

I made an effort to not consider other EPS or revenue estimates before formulating my own. In some recent quarters, my estimates have been more accurate than the consensus of stock analysts. [See Chart 1 and 2]

Possibly stock analysts are overestimating the expense of WWE’s return to touring or are overlooking the likelihood the company will recognize several million dollars in production incentives, the norm for Q3, which I’ve modeled as a $17 million negative expense. My understanding of comments from CFO Kristina Salen on recent earnings calls is that media expenses for the return to touring will be similar to those of 2019, when media expenses were lower than those associated with WWE’s elaborate Thunderdome presentation that was used instead of touring.

I estimated $273.9 million in revenue for the period of July 1 to September 30. The consensus is at $260.6 million, according to Seeking Alpha.

The projection that WWE would report $195 million in net income and more than $1.1 billion in revenue for 2021, would set annual company records, adjusted for inflation.

RETURN TO TOURING

Expect WWE to celebrate its best North American average paid attendance in many years. My estimate is 7,900, which would be the highest for a quarter since 2010 Q1. High attendance was driven by strong ticket sales early in the return and the Summerslam event in Las Vegas in August. The latter alone had about 45,000 tickets distributed. I anticipate total worldwide paid attendance for Q3 at 330,000 across 42 events. I assumed 10% of all tickets distributed, reported by WrestleTix, were comps, and the rest paid.

A Live Events division revenue estimate for Q3 is difficult to anticipate because it’s evident WWE benefited from “pent-up” demand as it returned to running shows with fans in attendance for the first time since March 2020. Results reported on Thursday also probably won’t be as informative about Q4 and future time periods.

I anticipate a profitable Q3 for the Live Events division, with as much as $7 million in operating income for a division that has struggled to show profitability in the last few years before the pandemic. However, I expect negative operating income for the division to return in Q4 as WWE runs more events than the prior quarter (about 56), and with lower attendances.

The first few events in July drew especially well. It’s likely WWE was able to charge higher ticket prices for these events in response to the increase in demand, but to what degree is more or less guesswork. The company will report the average price of tickets sold, broken down by North America and international regions, but those average ticket prices will look different going forward, in time periods with more relaxed demand. Indeed, some events in Q4 already appear to be struggling to move ticket sales. WWE offered discounted tickets in at least two markets recently, San Francisco and Long Island.

With the return of events WrestleTix has emerged as a fantastic resource, tracking activity on publicly-visible seating maps, and reporting ongoing counts of tickets distributed for events held by WWE, All Elite Wrestling, and other wrestling companies. My estimate of metrics related to live events largely rely on information from WrestleTix.

TV RATINGS

The return to touring clearly benefited television viewership of WWE’s flagship programs, Raw and Smackdown. Sequentially, total viewership was up 2% and 6% in Q3 for Raw and Smackdown, respectively, following four consecutive quarters of often double-digit sequential losses in viewers for both shows.

Raw and Smackdown averaged viewership in Q3 slightly higher than the prior year [Chart 3], a period when TV was produced in front of no fans and mostly before the Thunderdome was introduced. Raw is averaging well below its Q3 2019 numbers; Smackdown is slightly higher by the same comparison but in Q3 2019, Smackdown was on the USA Network, before the move to Fox with its higher reach.

Internal trends aside, WWE’s flagship shows remain among the most-watched programs on television, especially in the key ad demographic, with viewers aged 18 to 49. During Q3, Raw’s median rank among both broadcast and cable programming on Mondays was #4; Smackdown’s median rank on Fridays was #1. These programs deliver those results at the cost of about $1.7 million per hour of new content, in the case of Raw, and $2.0 million per hour in the case of Smackdown, likely on the low-end of the cost of comparable programming.

For one peer example, ESPN’s new deal with the NHL is reportedly worth an average annual value of $400 million, nearly twice as high as TNT’s deal with the league. ESPN gets about 118 games per year, which comes out to about $3.4 million per game. The season opener in October delivered a 0.38 P18-49, the best for a game so far this season, and a number that would be under Raw’s lowest ever (0.39). WWE charges $4 million and $5 million per episode of Smackdown and Raw, delivering an average demo rating in October of 0.57 for Smackdown on broadcast and 0.45 for Raw on cable. WWE is paid more per event than the NHL while delivering better in the demo, which suggests in my view WWE live broadcast rights are fairly-priced if (and it’s a big “if”) ad and carriage values for WWE and NHL are comparable enough.

AEW COMPETITION OUTLOOK

WWE is increasingly vulnerable to direct competition from All Elite Wrestling, which launched in 2019 and is funded by the Khan family, who also own the Jacksonville Jaguars. While WWE remains by far the leader in wrestling, it’s my long-standing belief the company will continue to cede market share to AEW for at least as long as Vince McMahon remains WWE’s CEO and head of creative. I believe McMahon has no plans to retire, nor does he intend to sell control of the company, despite what I view as weakly-supported speculation.

WWE’s greatest challenge in my view is the quality of its content and the direction of its creative, headed by McMahon. Management doesn’t genuinely recognize the problem, so they won’t meaningfully address it. The increase in value of live sports rights, which has benefited the sports industry in general, provides ample cover, driving WWE to set financial records.

In the meantime, AEW, a company I believe wouldn’t exist if WWE had been producing better quality content over the last five years, has managed to have its weekly program, Dynamite, on TNT essentially tie Raw in P18-49 in the same week on two occasions in September. AEW is also out-selling WWE in six markets currently in which both companies have upcoming live events.

WWE’s wide lead over AEW in total viewership is almost entirely driven by viewers age 50 or older, a group less valued by TV advertisers. However I believe WWE’s product is more appealing to kids. Suggesting WWE is still well ahead with kids, the company dramatically outperforms AEW on YouTube [Chart 4], albeit with a massive historical video library at its disposal. AEW is not seeing the year-over-year declines in views WWE is for the early pandemic months [Charts 5 and 6], possibly related to increased interest in AEW since the addition of former WWE stars CM Punk and Bryan Danielson.

But on a new platform, TikTok, WWE also has a huge lead. AEW has just 338,000 followers on TikTok, as of the end of October. WWE had 14 million, or 41x the number of AEW’s followers [Chart 7]. AEW actually went months with little or no activity on TikTok until this summer [Chart 8].

While AEW may be capturing young and middle-aged adults, WWE continues to outperform AEW on online video platforms. WWE also has a higher percentage of its audience who are women and people of color. Furthermore, while there’s a generation of wrestling fans (and talent) disenfranchised by WWE who may be attracted by AEW, there’s also a generation of fans who have embraced WWE’s brand of wrestling for what it is.

Disclosure/disclaimer: I do not currently hold any positions in WWE stock (NYSE: WWE) and have no plans to initiate any such positions. This article was written independently. It expresses my own opinions, solely. I am not receiving compensation for this article. This article is not and should not be construed as investment advice.

EDIT: This article has been updated to correct YouTube data that incorrectly showed higher view counts for WWE and more negative year-over-year growth for AEW.

[Chart 1] ^Jump back to where you where in the text

[Chart 2] ^Jump back to where you where in the text

[Chart 3] ^Jump back to where you where in the text

[Chart 4] ^Jump back to where you where in the text

[Charts 5 and 6] ^Jump back to where you where in the text

Source: socialblade.com

[Chart 7] ^Jump back to where you where in the text

[Chart 8] ^Jump back to where you where in the text

Brandon Thurston has written about wrestling business since 2015. He operates and owns Wrestlenomics.