This article was originally posted for subscribers last week Wednesday and included my full financial estimate model for WWE, not included here. Get access on Patreon.

Escalating media rights values should spur WWE to break its profit records for the third consecutive year in 2022. The tailwind from guaranteed live rights fees and incremental growth from other licensing opportunities more than offsets weakened fan interest that will keep consumer sales stagnant.

Even though popularity in the core product is down from recent years and possibly continues to wane, current viewership of Raw and Smackdown is strong enough to justify an increase in U.S. payments for new deals that would begin in October 2024.

WWE’s recent earnings call reported on the first full quarter since live event touring returned, indicating what normal trends might look like for the near future. I’m now expecting a record $206 million in annual net income for 2022 (up my earlier estimate of $190 million), adjusted OIBDA of $365 million (I haven’t previously estimated adjusted OIBDA), based on annual revenue of $1.25 billion (down slightly from $1.26 billion). Aforementioned differences are largely driven by what I believe is a lower, more accurate estimate of WWE Network revenue and lower expenses than I previously understood related to the operating and marketing of the company’s media and live events divisions.

Media rights value outlook for Raw and Smackdown remains strong

I believe the most important factor determining the value of Raw and Smackdown’s live rights is those programs’ performance with viewers 18 to 49 relative to other programs throughout television generally.

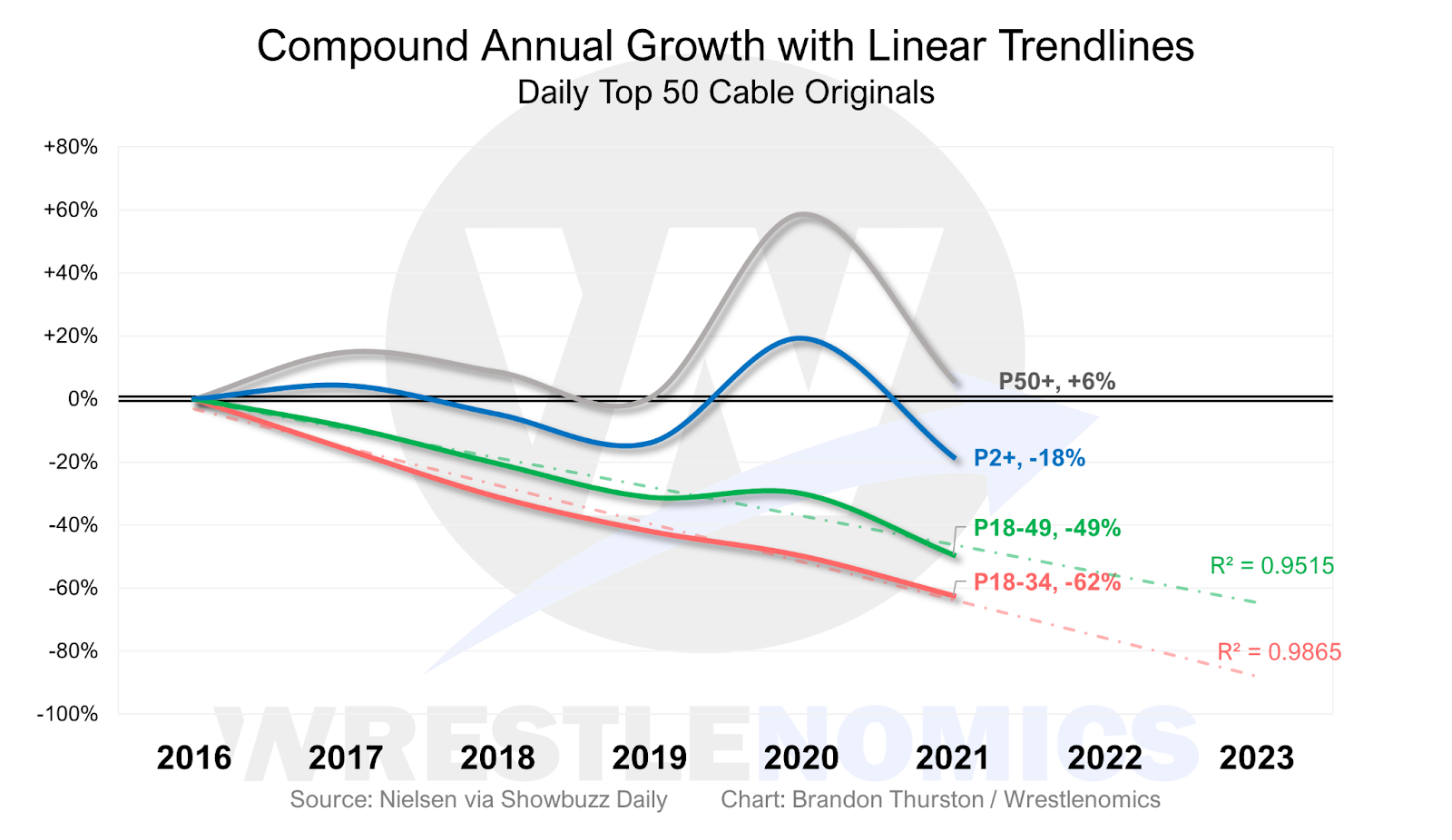

The average episode of Smackdown on Fox in 2021 had a P18-49 audience in the top 4% of all the year’s telecasts among cable originals and national broadcast airings, according to my analysis of Nielsen data from Showbuzz Daily [Chart 2].

By the same measure, the average episode of Raw was in the top 5%.

NXT, which I believe there’s far less value in, was in the top 24%.

For comparison, competitor AEW Dynamite was in the top 9%. AEW Rampage was in the top 12%, despite its 10 pm time slot.

It’s notable that WWE reality program Miz & Mrs. was in the top 13%, though it had just six new episodes in 2021; the other programs air new episodes year-round.

Despite declining viewership over the years, the trend in the percent rank for Raw and Smackdown hasn’t significantly weakened. Smackdown’s percent rank has only improved, coinciding with its move from USA Network to higher-reach Fox. Raw’s rank has weakened marginally but unpredictably from 2017, while remaining within the top 5%.

Will the reach of linear TV be enough for WWE through the late 2020s?

I expect WWE’s live rights in the next round to include some kind of live streaming component. To ensure WWE can broadly reach consumers including younger audiences, live distribution on linear TV may not be enough by the late 2020s.

Traditional TV viewership of the daily top 50 cable original telecasts for people aged 18 to 49 declined 49% from 2016 to 2021 and fell 62% for ages 18 to 34 [Chart 3].

That said, even while linear TV viewing is in decline and skewing older in age, traditional TV still makes up the majority of TV use time in the U.S., while streaming accounts for a little over 25% of that share.

Reach is even more important to WWE than to other major U.S. sports leagues, where local markets support individual teams and most games are telecast as regional broadcasts. WWE needs high-reach availability nationwide and weekly to support live event touring and consumer products businesses.

Tentatively, I think the likely outcome is the same company holding streaming and linear rights for the given show: for example, NBCUniversal’s entities USA Network and Peacock holding rights to Raw. Opposing companies may be unwilling to compete with one another, i.e., one company holding streaming rights (e.g., Prime Video) and a different company holding linear (e.g., USA Network), in case one of the platforms ends up empty-handed as behavior shifts (or doesn’t).

If this assumption is accurate, it puts Fox holding onto Smackdown more in question. Fox lacks a suitable streaming platform. Fox-owned Tubi (a low-revenue FAST) and Fox Nation (the streaming extension of Fox News) aren’t sensible options.

Content owners like WWE hope major tech companies like Amazon, Apple, and Netflix become new bidders for their rights. However, none of the tech players currently own a linear network, and therefore lack both kinds of media platforms WWE might need to navigate the late 2020s. A major acquisition that actually passes antitrust scrutiny (like, say, Amazon buying NBCU away from Comcast) or, perhaps more likely, a partnership between a tech player and a traditional network, could change these dynamics.

A third large-scale international event?

WWE president Nick Khan hinted at a third “large-scale international” event on the last earnings call. “Large-scale international event” is the company’s euphemism for its controversial events in service of the government of Saudi Arabia, but it was hinted to me that Khan wasn’t referring to a third event for the kingdom, which would be a significant financial revelation since each Saudi event is worth $50 million in payments to WWE.

Instead, I expect WWE will announce a stadium event in Europe, most likely in the United Kingdom, for the monthly premium live event in September. The schedule the company released in October 2021 shows an event during Labor Day weekend with the location listed as “TBD”. The U.K. hasn’t had a true pay-per-view/premium live event since Summerslam 1992. A peak monthly event in the U.K. would carry historic weight with fans in the region and would be a hot ticket. Putting such an event in a stadium-sized venue is probably optimal for the kind of demand it would attract. Therefore, I modeled into Q3 $5.9 million in incremental live event revenue. Such an event would positively impact venue merchandise in the quarter also.

A major event on Labor Day weekend would also compete for fan attention with one of All Elite Wrestling’s quarterly pay-per-views. AEW’s All Out event has been held during that weekend each year since 2019. AEW has more to lose in such a situation as it more heavily relies on direct-to-consumer activity by way of pay-per-view sales at a $50 retail price in the U.S. Conversely, WWE’s premium live (née pay-per-view) events are primarily streamed to viewers at a fraction of the cost to the consumer, on Peacock domestically and the WWE Network internationally. Ticket sales for the Labor Day weekend events wouldn’t strongly compete with each other since they would be on different continents. I expect All Out 2022 to be in Chicago, as it was last year and in 2019.

Stagnant consumer interest

WWE had a great Q3 2021 for live events, one of the best quarters for the division in company history, benefiting from pent-up demand as touring returned in mid-July. Since then, ticket sales for WWE’s most frequent events, non-televised house shows as well as tapings for Raw and Smackdown, continue to decline [Chart 4].

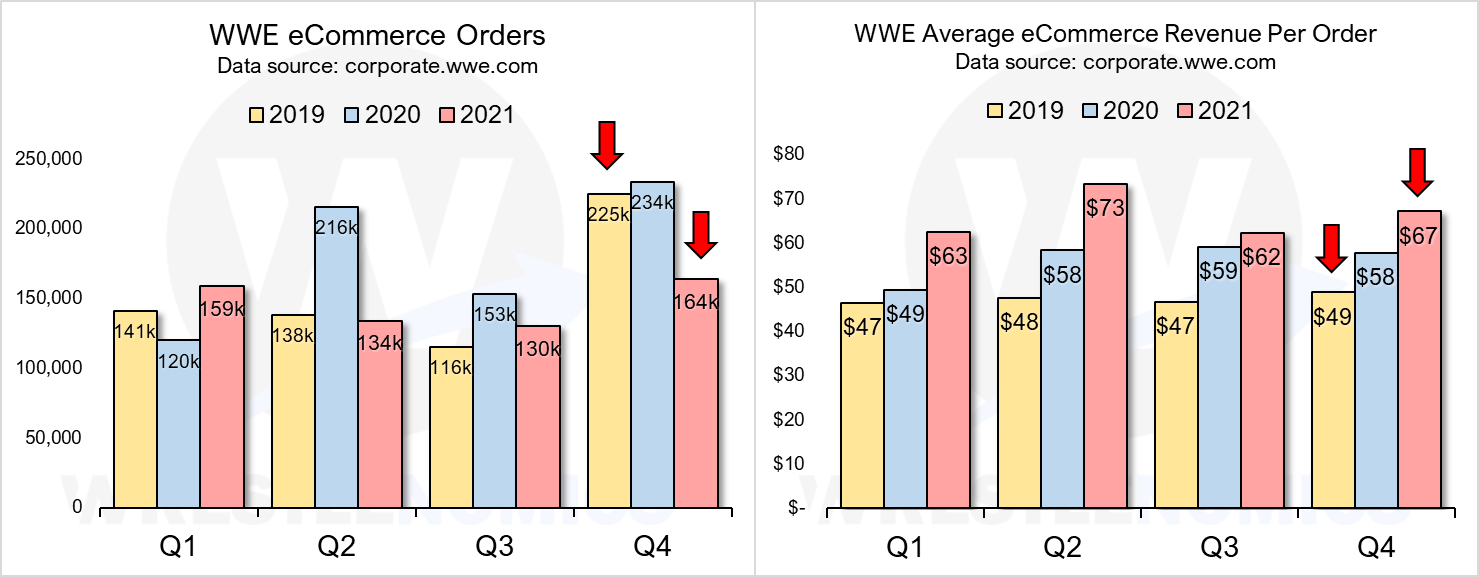

Another indicator of consumer interest is eCommerce sales. Those surged during the interruption of touring, somewhat offsetting the loss of venue merchandise sales. In the first full quarter comparison since touring resumed, eCommerce sales in Q4 2021 were even in revenue from Q4 2019 (the most recent pre-Covid Q4), but 30% lower in order volume. Fortunately, the company managed to increase revenue per order by 37% from two years ago, counteracting the decrease in transactions [Chart 5].

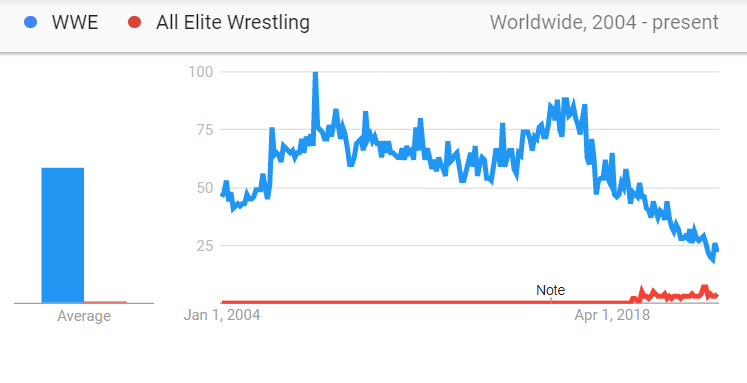

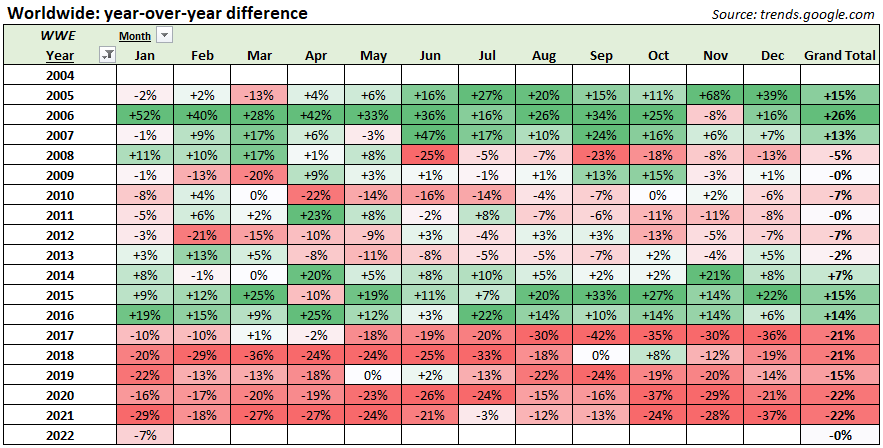

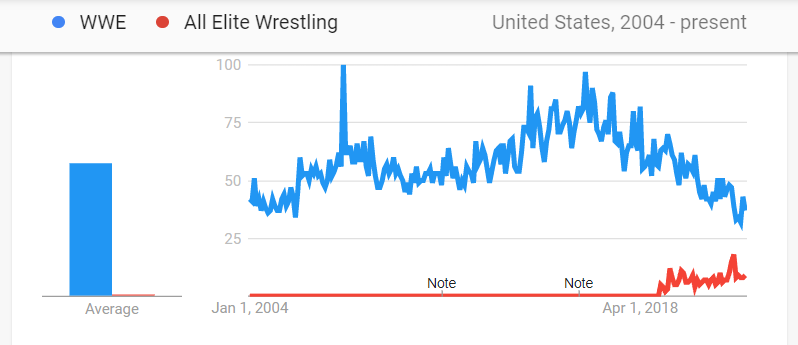

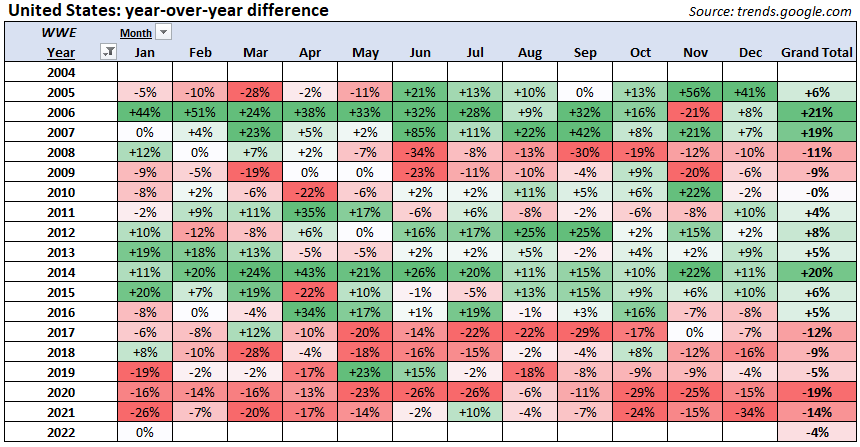

Google web search, which I view as an indicator of name recognition and mindshare, continues to be in secular decline for WWE, worldwide and in the U.S., for most year-over-year monthly comparisons since 2017 [Chart 6, 7, 8, 9].

I believe WWE’s fan base has deteriorated because of the poor quality of the core content, primarily due to creative leadership of CEO Vince McMahon. New major stars haven’t been more fully developed and storylines are weakened due to a lack of long-term creative planning, inauthentic presentation, misevaluation of talent, repetitive matchups, among other issues.

Management doesn’t acknowledge any problem with creative. McMahon is reportedly dismissive of criticisms of the content, citing the company’s financial success. Khan’s prepared statements in earnings calls only allude to a “strong in-ring product”.

Challenges with consumer interest are obscured by WWE’s increasing and largely guaranteed revenues from business relationships, a dichotomy that continues to become more defined as contractual escalators increase payments while the fan base diminishes under McMahon’s creative direction.

Disclaimer/disclosure: This article expresses my personal opinions only. I do not currently, nor have I ever, held stock positions in World Wrestling Entertainment, Inc. (NYSE: WWE). I have no plans to initiate any such positions within the next 72 hours. I am not being compensated for this article or any of my other Wrestlenomics-related work except through audience-driven revenue, including Patreon subscriptions and programmatic advertising.

This article is not investment advice, nor should it be construed as investment research.

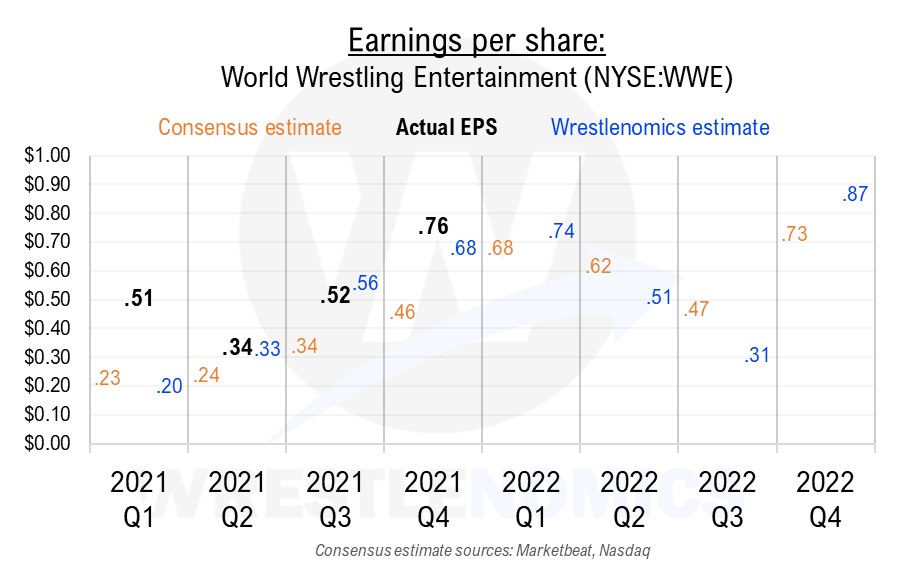

↓ Chart 1: My recent history estimating EPS

↓ Chart 2: Compound Annual Growth with Linear Trendlines

(Jump back to text)

↓ Chart 3: P18-49 Viewership Percent Rank: Calculated Annually

(Jump back to text)

↓ Chart 4: Estimated Tickets Distributed, by Event Type

(Jump back to text)

↓ Chart 5: WWE eCommerce Orders and WWE Average eCommerce Revenue Per Order

(Jump back to text)

↓ Chart 6, 7, 8, 9: WWE Google Web Search Trends: Worldwide and United States

(Jump back to text)

Brandon Thurston has written about wrestling business since 2015. He operates and owns Wrestlenomics.