Note: I decided to start not including the calculated “non-P18-49” columns in the table below because I feel it’s not that informative relative to the space it takes up. If enough readers request that I bring it back, I will consider it.

The preliminary rating for WWE Smackdown on Fox last night was 2,390,000, according to SpoilerTV and Programming Insider, although TV Series Finale shows a lower number, 2,290,000.

Assuming 2,390,000 is the correct fast affiliate measurement, we project the final total viewership for Smackdown to be about 2,520,000 viewers, based on our analysis of consistent differences between the fast affiliate and final rating over the last twelve months.

The final rating should be reported on Monday afternoon.

If our projection is accurate, total viewership last night was on the level of two weeks ago, the night before the Royal Rumble when Smackdown was watched by an average of 2,544,000 viewers.

Another number of around 2.5 million viewers would continue Smackdown’s trend of delivering higher viewership than during the same period last year. Smackdown’s average viewership for February 2022 was 2,167,000.

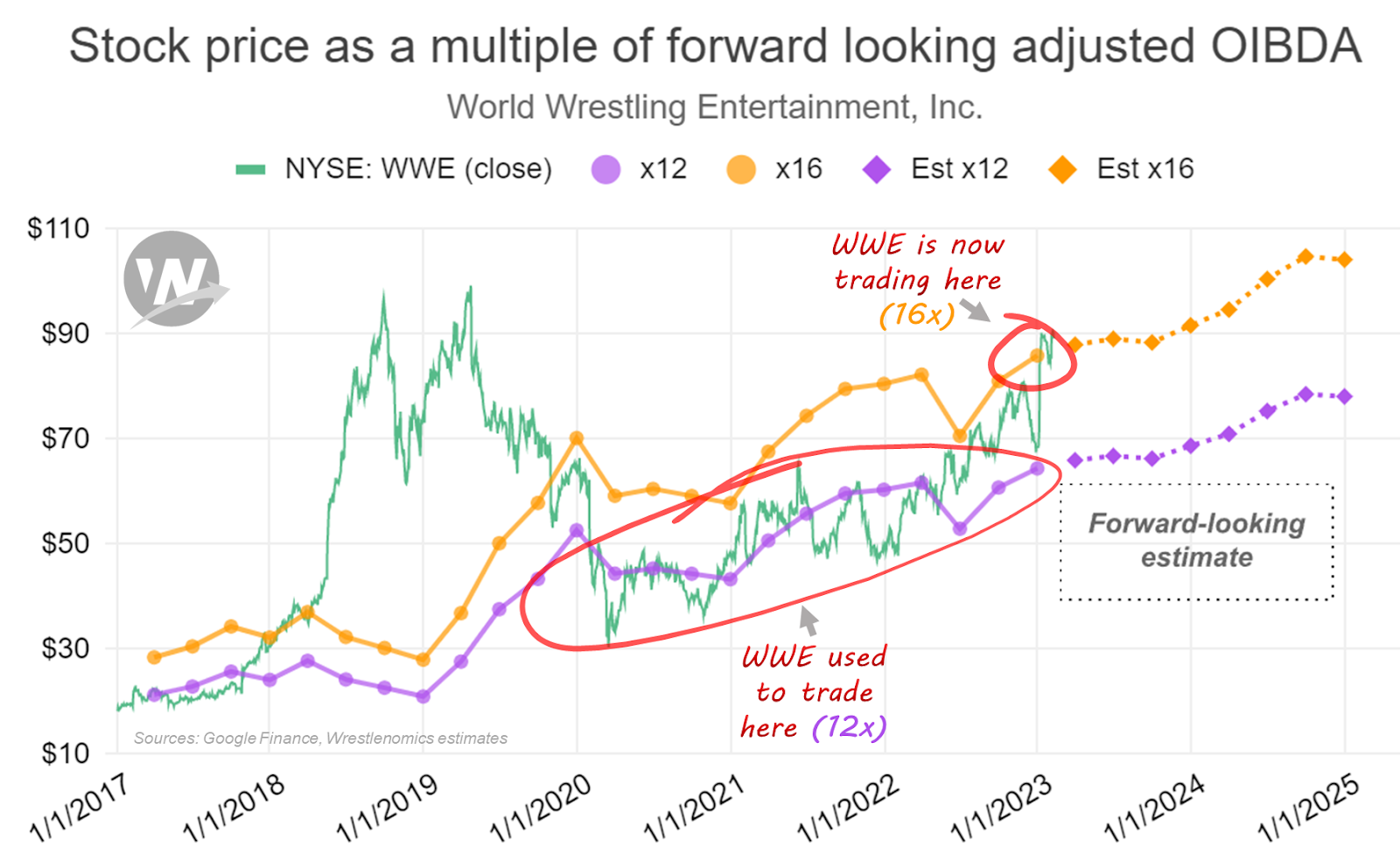

WWE’s current valuation, hovering around $90 in recent days, is nearing the fringes of plausibility.

The market apparently believes the company could be bought at almost $7 billion. Traders seem to be overestimating the demand, imminence, and, indeed, the likelihood of such a deal.

[ppp_patron_only level=”5″]

CEO Nick Khan’s assurances that founder Vince McMahon may accept a transaction that pushes him out of the company, may soothe some investors but his words are carefully chosen.

“He’s one hundred percent open to a transaction where he’s not included in the company moving forward,” Khan said Friday on CNBC.

The idea that Vince would put shareholder interests first sounds reasonable on its face. After all, he is the largest shareholder. He holds around $2.5 billion worth of WWE stock, probably the majority of his personal wealth.

But my belief is that Vince values power within the organization he controlled for decades more than any dollar amount. If he truly cared more about shareholder interests, it would’ve been wiser to not force his way back onto the board as executive chairman, against the wishes of the directors. WWE was a more attractive asset in late 2022 when it was more removed from Vince’s aura of scandal and unpredictable influence. If getting the best deal was the greater concern for him, he could have participated as a shareholder only.

His stated intention, that he insisted on returning to the board to explore a company transaction, isn’t particularly convincing and may be little more than a cover to avoid investor resistance while serving to provide a media distraction as he returned to the company five months after resigning in light of multiple sexual misconduct allegations and a related investigation.

Vince is open to a deal that leaves him out, Khan says. What kind of offer it would take to actually get him out of the company is another question.

The notion that any major media conglomerate is in serious pursuit of owning WWE is flimsy.

CNBC anchor David Faber told Khan, on the air on Friday, that Comcast is unlikely a realistic buyer. That aligns with my belief Comcast CEO Brian Roberts is unlikely to approve of an acquisition of WWE, given the cultural stigma of wrestling, the expertise needed to oversee such a business, and — a late addition — the newest bad press and possible family drama surrounding Vince. Those risks offset the prospect of putting a cap on the escalating price of WWE content that NBCU platforms USA Network and Peacock rely on.

The likes of Amazon and Disney may have similar reservations as Comcast. Netflix had no comment on a potential buyout and executives are confident they can create valuable IP rather than purchase it. Acquiring a several-billion-dollar asset would be inconsistent with Warner Bros. Discovery’s strategy of keeping costs down and addressing the debt taken on from its recent merger. WBD seems invested in WWE competitor AEW, additionally, which I believe the media company holds a minority stake in. Fox, which airs Smackdown, lacks the variety of media platforms needed to fully monetize WWE content. And the Murdoch-owned company may be staying lean to deal with their own company transactions anyway.

That leaves Endeavor or, more likely, an action to take WWE private.

There are clear synergies with Endeavor. A move to separate Endeavor sports properties like UFC and Professional Bullriding into a merger with WWE could make sense. Making Endeavor’s talent agency and streaming businesses their own separate publicly-traded entity may end up with those assets being valued more highly than they are currently. Khan and Endeavor CEO Ari Emanuel are likely friendly enough to get those talks started.

In Endeavor’s case, though, I’m skeptical Emanuel will accept a deal that gives Vince the opening to regain the power that he wants. Further, major Endeavor investor, Silver Lake, may be reticent to approve of a transaction that results in it gaining stock that has only a moderate prospect of growth in its future.

Vince’s best chance to remain in power at WWE may be in a group action to take the company private with sovereign wealth involved, in the form of the Saudi Arabia Public Investment Fund. Reportedly, the PIF bid strongly to try to acquire Formula 1, and WWE would probably cost the Saudi government less than the auto racing organization.

In the case of a take-private action, it doesn’t seem automatic that new owners would be willing to let Vince keep control, at least over the long term, which ultimately could prevent a deal from being completed.

Khan’s suggestion that a sale could happen within the next three months is likely meant to create urgency and to get clarity on WWE’s strategy in the event a sale isn’t happening and the company needs to move toward getting the best possible deal for a renewal of domestic live rights to Raw and Smackdown, which currently account for around one-third of WWE revenue.

When trading rationally, WWE has been valued at around 12 times its forward-looking profitability. The exception was the delirious period from early 2018 to mid-2019 when a great new U.S. TV deal led the market to think live rights value would fall from the sky around the rest of the globe, that India would come in hot, and perhaps the U.K. would renew at an upgrade. WWE’s new friends in the Saudi government who controlled a partner network in the Middle East North Africa Region would probably give them a nice raise, too.

None of that happened. Sony in India doubled WWE’s deal, which was actually a mild disappointment. In the U.K., Sky ended their multi-decade relationship, leaving WWE to go to BT Sport and Channel 5, taking a deal with lesser reach and seemingly lower fees. And negotiations in the MENA region with sovereign-backed MBC were strung along, then ended up being the subject of a shareholder class-action lawsuit (and subsequent settlement), until a deal was finally done in 2022 to minimal fanfare.

Now with the hope of a sale at a premium, the stock is near $90, trading at 16 times forward-looking profitability.

Without a multitude of serious potential buyers, WWE’s current price is lofty. And if no company transaction takes place, shares are bound to correct back down to the $70 to $75 range they came from.

If this article was for a mainstream publication, it would probably have to end with a line like, “What Wall Street is buying may only turn out to be Vince McMahon’s latest storyline.”

Disclaimer/Disclosure: This article expresses solely my own opinions. This article is not intended to be investment advice, nor should it be construed as such. I do not currently, nor have I ever held positions in WWE shares (NYSE: WWE). I do not currently hold positions in any other company mentioned in this article.

[/ppp_patron_only]

Brandon Thurston has written about wrestling business since 2015. He operates and owns Wrestlenomics.