For anyone in the U.S., Peacock Premium becomes the exclusive home for WWE Network content, beginning April 4. It will be the end of an era of business for Vince McMahon’s company, which seven years ago boldly launched its own streaming service.

So let’s reflect. Did it work out? Is WWE more or less profitable today because of the Network? Is the sale of the domestic rights a sign of failure? Could it have turned out differently? I’ll try to answer those questions here.

There are a few signs the WWE Network was a disappointment, including:

- The WWE Network, as implemented, has not produced an obvious positive return on the investment, in my estimation. I will explain further in this article.

- Subscriptions plateaued around 1.6 million by 2019, well short of WWE’s public goal of 3 million.

- Former co-presidents, George Barrios and Michelle Wilson, the architects of the Network strategy were abruptly terminated in January 2020, at the same time WWE made clear it was interested in selling the rights to the Network content and discarding the direct-to-consumer model.

What we need to know about WWE Network profitability

Figuring out whether WWE is more or less profitable today because of the Network is ultimately hypothetical. To do so, we have to conceive of at least one alternate scenario and compare it to WWE’s actual financial performance during the years in which the Network existed.

It’s important to understand a few points when thinking about the WWE Network, which makes concluding the company made a positive return on this investment more difficult:

- The WWE Network cannibalized the pay-per-view business, as many people are aware.

- It also cannibalized DVD/Bluray, digital VOD sales, and internet pay-per-view sales.

- An issue often overlooked: The timing of the WWE Network launch negatively affected WWE’s TV rights negotiations that were ongoing in early 2014. Vince McMahon confirmed this publicly.

- The WWE Network required around $66 million in start-up expenses. These expenses were incurred beginning as early as 2011, according to company public filings, which raises the financial benchmark for a positive return on investment.

- But there were benefits too. The Network allowed the company to sell more ad inventory and increased the number of viewers who saw sponsors on monthly peak events.

- A vast amount of data was collected since millions of user accounts were created, which allowed for targeted marketing. However WWE’s attempts at selling wrestling fans’ data to third parties was disappointing, I’ve been told.

- And you could write a whole other article on the potential opportunity WWE may have had in growing a video streaming business (much like its shuttered WWE 24/7 and Classics On-Demand business) that attempted to monetize the company’s video library but didn’t include live broadcasts of monthly PPV events.

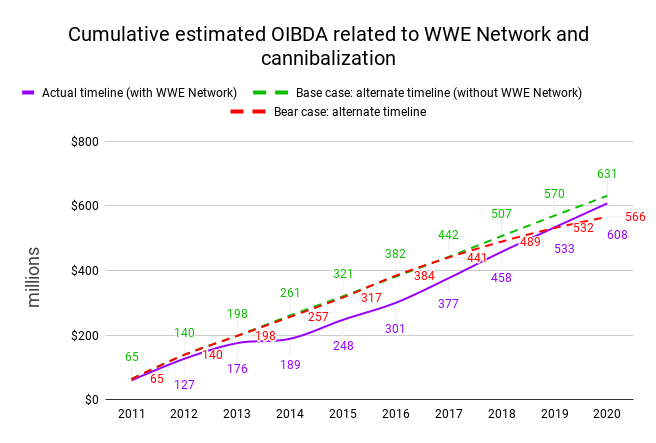

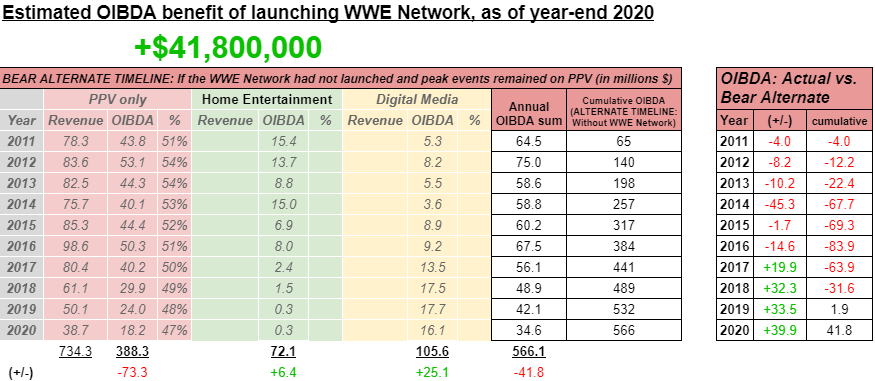

Later on in this article I’ll show the results of my estimates about what WWE’s profitability could’ve been, in an alternate timeline, if the WWE Network was never launched, compared to my estimates of the company’s profitability in our actual timeline. Profitability is here measured as OIBDA (operating income before depreciation and amortization).

This estimate is somewhat further complicated by the fact WWE changed its financial reporting method after 2017, requiring me to do estimates on the actual timeline as well as the hypothetical “alternate” timelines.

To come up with a likely scenario where the WWE Network is a financial winner, I have to imagine a “bear case” alternate timeline in which pay-per-view demand from 2014 to 2020 severely declines.

Alright, let’s try to do the math

Following these graphs are the key assumptions behind them.

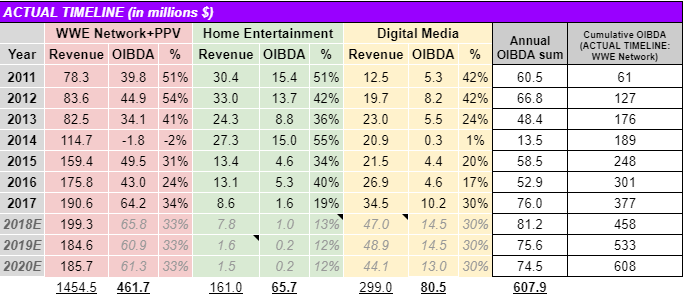

For the “actual” timeline, we have actual OIBDA details in the segments shown in the above column graph reported by WWE for the years 2011 to 2017. Because WWE changed its reporting method thereafter, estimates had to be made for the years 2018 to 2020. The key assumptions for those later years were:

- WWE Network OIBDA margin of ~33%

- Digital Media OIBDA margin of ~30%

- Digital Media revenue equivalent to ~67% of media ads & sponsors revenue.

- Home Entertainment OIBDA margin of ~13%. Revenues less than $2 million, beginning 2019.

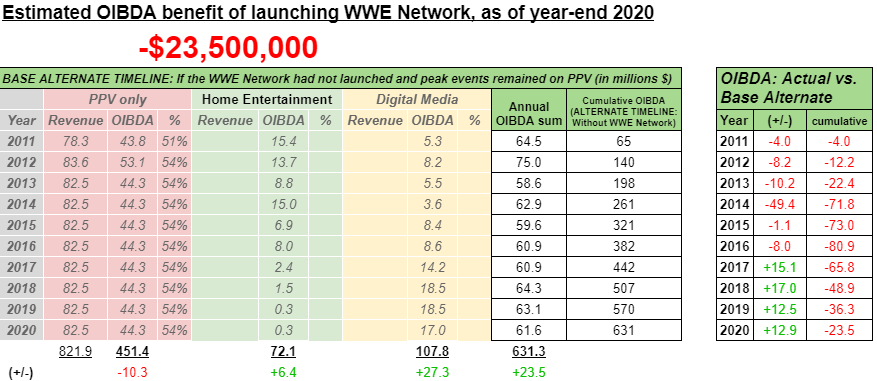

For “Base case” alternate timeline, the key assumptions were:

- Traditional PPV generates ~$44 million in incremental annual OIBDA, 2013 to 2020

- Internet PPV generates ~$4 million in incremental annual OIBDA, 2014 to 2020.

- Home Entertainment OIBDA at a rate of ~1.5x of actual timeline, beginning 2015.

For “Bear case” alternate timeline, the key assumptions were:

- PPV and internet PPV sales and profitability decline over time, consistent with worldwide Google search trends, resulting in $63 million less (-14%) lower OIBDA from pay-per-view.

- Same Home Entertainment assumption as “Base case”.

Below are revenue and OIBDA estimates tables for the three relevant scenarios: “actual”, “base alternate”, and “bear alternate”.

You’ll notice I didn’t deal with the benefits of ad revenue or the value of user data, mentioned earlier, in these models. WWE’s filings don’t give us much clue on how to calculate those values. I tend to believe those factors’ accretive OIBDA is relatively low on the scale of the calculations made here, but maybe it makes the difference of a few million in OIBDA.

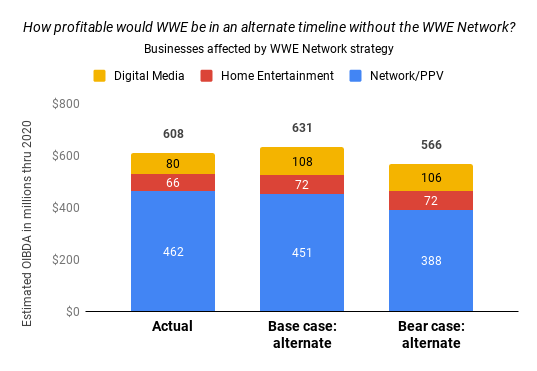

If we accept the “bear case” conclusion that the WWE Network added about $42 million in OIBDA for the company, that would mean the WWE Network meant, at best, a 5% increase in OIBDA over the entire Network era. WWE generated about $915 million in total company OIBDA in the years from 2011 to 2020.

In this generous “bear case”, the Network provides a small incremental increase in profitability, but not the kind of “transformational” change that was hyped at the product’s launch.

So why didn’t things turn out better?

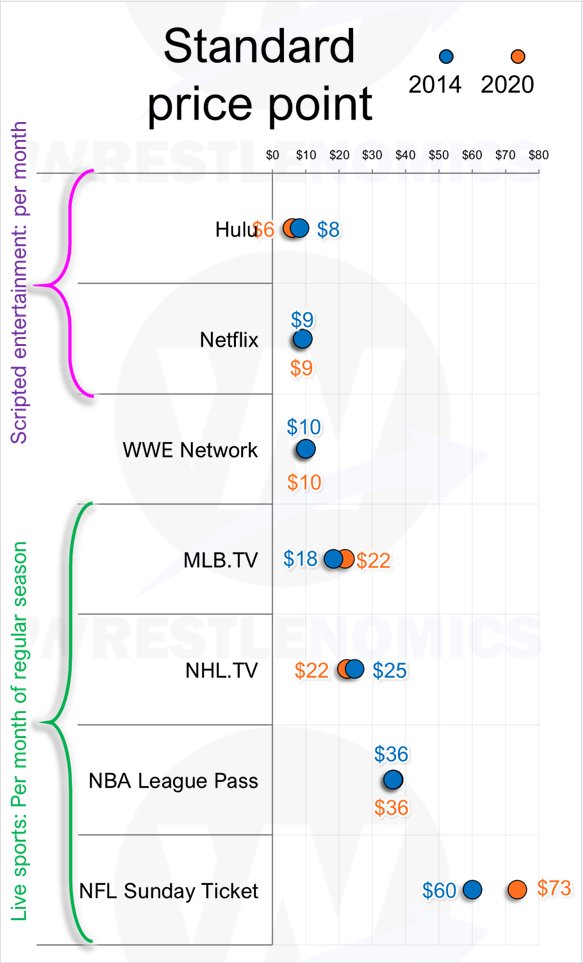

The $9.99 price point was too low, possibly because WWE executives misunderstood the product’s place in media In pricing the Network, WWE placed itself nearer to scripted entertainment pricing than sports. In hindsight, $15 or $20 monthly would’ve been more appropriate.

At the time of the Network’s launch as well as today, sports leagues charge their fans higher prices for access to out-of-market games. That’s especially evident if you average the annual cost only over the months in which the league operates its regular season, as shown in the “Standard price point” chart above.

Per month of its regular season, MLB charged $18 in 2014. The NFL went as high as $60, and higher today. Yet in its domestic market WWE in 2014 and until it transfers rights to NBCU in 2021, charged subscribers just $10 monthly — more along the lines of the monthly fee for services like Netflix or Hulu.

So why did WWE price its service at $10, more like a scripted entertainment service and less like a sports streaming service?

Since Vince McMahon took control of the company in the 1980s, he’s worked hard to move his wrestling product toward being seen as “show business”, entertainment rather than sport. I think one of the core impediments for WWE growing its consumer revenues is McMahon’s unwillingness to embrace his product for the simulated sport that it is. Usually, that flaw only manifests in onscreen creative. McMahon is normally an effective corporate leader, eager to bet on new media like cable TV, pay-per-view, social media, or streaming. But in this case, his philosophy of imagining WWE “not as sport but as family-oriented sports entertainment” may have been a detriment to corporate strategy, too.

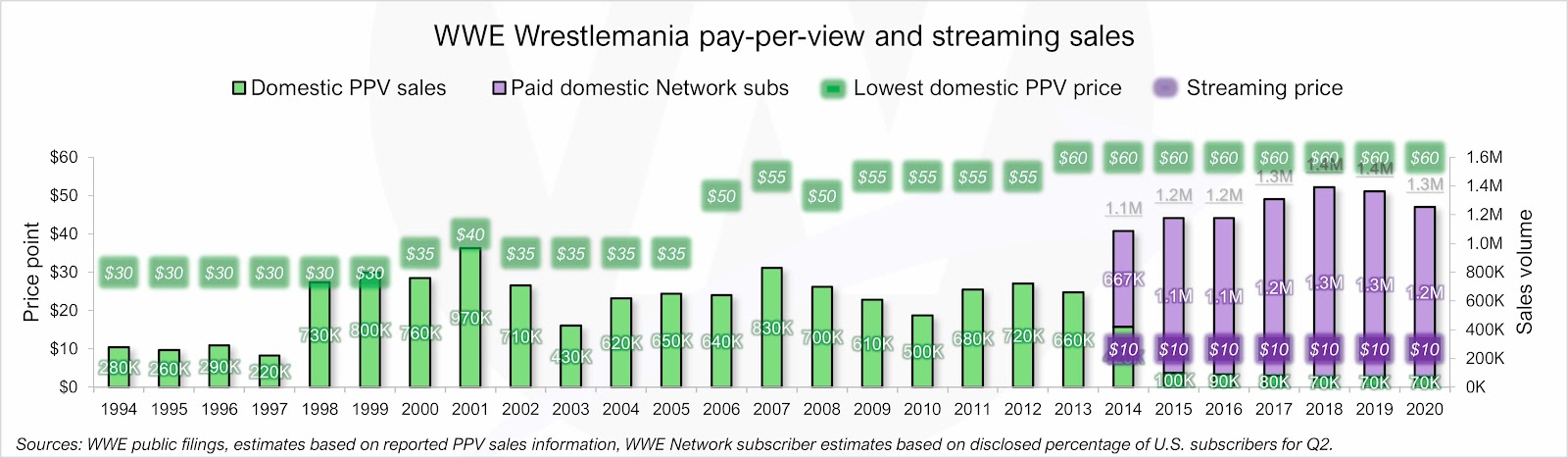

Pay-per-views were sold at a variety of price points for many years and it didn’t seem to have a strong effect on sales. The PPV price of the biggest show of the year, Wrestlemania, nearly doubled in price from 2005 to 2013, gradually increasing from $35 to $60. It’s not clear price increases affected demand.

It’s much more likely, in my view, whatever affected the change in Wrestlemania PPV sales from year-to-year had much more to do with the hype around the matches on the event. It was a good business decision to raise the PPV price on Wrestlemania (and on PPVs generally).

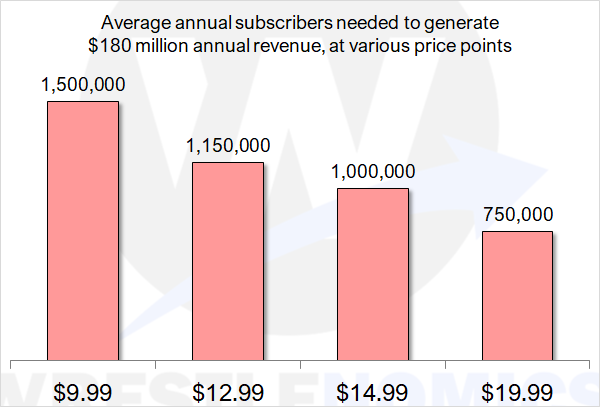

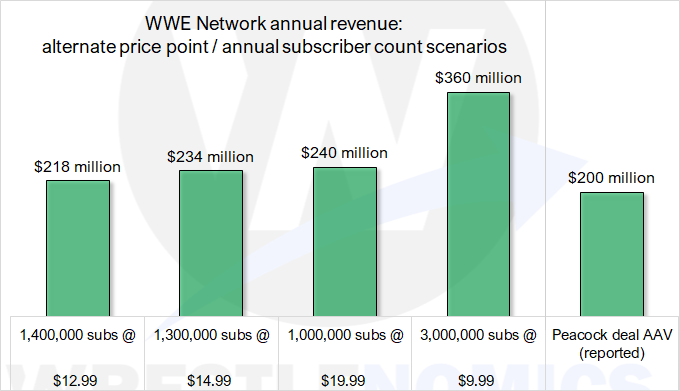

To illustrate a point, if the worldwide monthly WWE Network price was about $20, paid subscribers could have been half of the actual achieved number (about 1.5 million) and generated similar revenue.

1.3 million subscribers at $15 monthly would generate $234 million annual revenue, almost 30% more than the actual performance of the Network in 2020, and edging out the average annual value of the new Peacock deal ($200 million). This hypothetical $234 million, though, is far short of WWE’s original goal of 3 million worldwide subscribers at $10, generating about $360 million in revenue.

In retrospect, as we explored earlier, it’s likely value was lost by essentially underpricing $60 PPVs at $10 for seven years. That lost value can hardly be regained. The Peacock deal (worth an average of about $200 million per year) salvaged the value remaining in PPV events by guaranteeing incremental revenue over a direct-to-consumer subscriber business (generating around $132 million domestically per year) that fell stagnant. Trying to put the genie back in the bottle and revert to a la carte sales of monthly events at a high price point would likely be met with resistance. I think it would present a massive friction point for a significant number of regular customers. WWE and NBCUniversal apparently recognize the old model can’t be reverted to at this point, given the decision to keep monthly PPVs as part of a low monthly fee.

Disenfranchised wrestling fans who would like to see WWE face economic consequences for perceived bad creative, is a sentence this media economy, with its need for live sports, never serves. Better developed stars and creative would’ve helped Network subscriptions, for sure, but the Network disappointed more due to strategy than creative.

The fault of the WWE Network was that executives didn’t recognize that wrestling is maybe the only medium on Earth that so overlaps sports and scripted entertainment. And if you understand that peculiarity, you’ll better understand wrestling price points, DVR viewing, linear viewership, broadcast rights, and probably more.

Final answers

Is WWE more profitable today because of the Network?

It’s a hypothetical question, but the answer isn’t an obvious ‘yes’. The Network as a business was more profitable than the previous pay-per-view business in isolated years, but the Network’s startup costs and cannibalization of other businesses offset much of the financial benefits for the duration of of the service’s run as a mainly direct-to-consumer product.

Is the sale of domestic rights a sign that the Network failed?

It’s a sign that it didn’t work out the way it was expected to. Executives had lofty subscriber goals that the Network fell well short of. By 2020, subscribers didn’t look like they were poised to grow much further. Raising the monthly fee would be risky. Selling rights to the content to a larger media company looking to invest in streaming at a higher scale is likely the better way to grow revenues related to the content.

Could it have turned out differently?

Certainly. In hindsight, I think the Network was obviously underpriced. I think a lower but not-that-much-lower number of subscribers could’ve been captured at $15 or even $20 monthly. Or access to the full library could’ve been part of a higher-priced premium tier. Or the most popular pay-per-views could’ve been left off the service and continued to be sold for $60 while still monetizing the library and other new content via streaming, which might’ve generated greater profitability.

Brandon Thurston has written about wrestling business since 2015. He operates and owns Wrestlenomics.